Hiding from reality

“They deem

him their worst enemy who tells them the truth.”

—Plato

“In an age of universal deceit,

telling the truth is a revolutionary act.”

—George Orwell

There are some condos that are so poorly managed, so poorly

maintained

and are in such serious financial troubles that they are virtually

bankrupt and yet the directors and some of the owners feel that,

although they are having some short-term difficulties, all is well.

There is nothing to worry about.

How

bad can it get?

In the west end of Toronto, there is a condo apartment tower that has

had water penetration through the building envelop since it was built

30-odd years ago. The builder gave the corporation some money as

compensation but that money was not spend on repairs so the leaks were

never fixed. Now, a third of a century later, about a third of

the units have serious water leakage and mould problems. (All of the units are on the east side of the building.)

The building has a serious cockroach infestation problem that

is being

ignored and the corporation is not paying its shared facilities expenses. The utility

bills and the contractors are paid late.

The reserve fund is woefully inadequate and is regularly tapped to

support the operating deficit. The roof anchors are unsafe and the

board needs to spend $500,000 to $1,000,000 to fix the exterior

brickwork. They have around $13,000 in the Reserve Fund but the board

tells the owners they have $300,000.

This year (2012) they had an AGM, after not holding one for the last

two years, and they have released no audited financial reports in the

last five years. The owners don't know how bad the situation is and

their board doesn't want them to know.

Yet, with all their problems, the two-bedroom units sell for over

$250,000. The purchasers see a pleasant looking front lobby, clean

elevators and clean hallways so they think everything is in order.

Their real estate lawyers don't pick up on the bad financial situation

that is described in the

status certificate and there are no warning signs of trouble until

after they have moved in.

How

do they get away with this?

The board hired a small property management company that is happy to

have a contract. Then they tell the owners that

they can't provide audited financial statements because the previous

managers

lost or destroyed the records.

Very cute!

Who

benefits?

The low-income owners who want low monthly fees. The board refuses to

listen to the

manager when he tells them that the monthly expenses must be raised and they

need to

arrange for a loan or special assessments to make the necessary

repairs. If the manager gets too insistent, they will replace him.

Why

they won't listen

The owners do not want to pay, or can

not afford to pay, an extra $30,000 per unit in special assessments, or

a loan,

plus pay extra monthly fees to maintain the property.

Most of the seniors and low-income owners strongly support the board

because their fees have not been increased for the last seven years so

the board has a lot of support.

How

can this go on

The disgruntled owners are too few in number. They do not have the

necessary political support to remove the board nor do they have the

money to take the corporation to court.

Further more, the owners are split into different ethnic groups so they

have trouble

working together. The owners know that the condo is not being run

well but they have no idea how bad things really are.

There are a lot of seniors in that condo and more than anything, they

want—or need—their fees to stay low.

Finally, no one wants the real estate agents, potential buyers or the

banks to learn the true condition of their building as property values

will sink and they could lose up to two-thirds of their equity.

The smarter owners—the ones who can afford to leave—are selling, one

owner at a time. Many are stuck there because they do not have enough

equity to buy elsewhere.

Eventually, the city inspectors will be made aware of the water

penetration problems and they will issue work orders. That is when the

board, and the owners, will be forced to fix their problems.

Chickens

coming

home

Eventually, the blindfolds must come off and as the owners at Las

Brisas, an aging condominium highrise on Bathgate Drive in Ottawa found

out in December 2013, reality can be quite a shock.

They got hit with a $53 million special assessment, roughly $40,000 to

$66,000 per unit.

Time is

running out

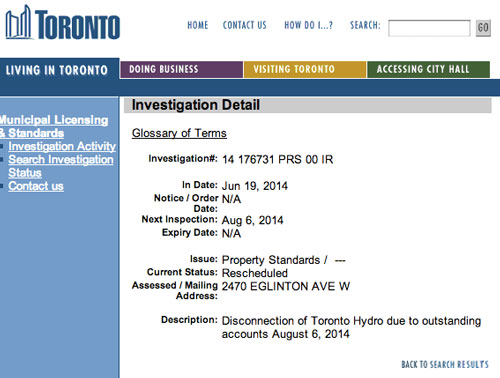

A posting on the

city's website

It looks like this condo's financial problems are catching up to them.

This is the second time in two years that the city has threatened to

disconnect their hydro unless they pay up.

What

can be done

Anyone in the market for a condo needs to be aware of the dangers of

buying into a troubled building. Reading and following the buying tips on this

website could help keep an

informed purchaser from buying a lemon.

top contents chapter previous next